- Key Takeaways

- DGRO's Dividend Growth: Separating the Quarterly Signal from the Annual Trend

- Why the Morningstar Methodology Creates This Outcome

- How SCHD's Quality Screens Produce Faster Income Compounding

- The Total Return Case for DGRO — and Why 2026 Is Different

- The March 2026 SCHD Reconstitution That Changed the Picture

- Three Rotation Paths and the Tax Strategy Most Investors Skip

- Which Dividend ETF Belongs in Your Portfolio?

- Watch the Full Breakdown on YouTube

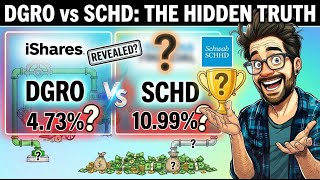

DGRO's 2025 annual dividend per share grew by just 4.73%. That single number tells a story most dividend investors have not yet noticed — the quarterly payments still land on time, and the fund still appears healthy on the surface. But measured against SCHD's ten-year dividend compound annual growth rate of 10.99%, DGRO is growing its income at less than half the pace of the fund most investors use as their benchmark. Understanding why that gap exists, what the data actually shows, and how to respond is what this analysis covers.

Key Takeaways

- DGRO's full-year 2025 dividend grew just 4.73% year-over-year, compared to SCHD's ten-year compound annual growth rate of 10.99%

- The Morningstar US Dividend Growth Index's five-year consecutive growth hurdle allows slow-growing mega caps to qualify and drag down overall distribution growth

- On a $50,000 investment, SCHD currently generates approximately $640 more in annual income than DGRO

- Over ten years, DGRO has outperformed SCHD on total return — roughly 290% vs 263% — largely due to growth-tilted holdings in Apple and Microsoft

- SCHD's March 2026 reconstitution has widened the year-to-date performance gap to roughly 11 percentage points

- A partial rotation rather than a full switch is the optimal path for most investors, with the right allocation tied to investment phase

DGRO's Dividend Growth: Separating the Quarterly Signal from the Annual Trend

One source of confusion around DGRO's recent performance involves the difference between quarterly and annual comparisons. In Q1 2026, DGRO paid 33.11 cents per share — a 6.5% increase over Q1 2025's payment of 31.09 cents. On a same-quarter year-over-year basis, the fund is still growing. Claims suggesting DGRO stalled year-over-year are not accurate when a single quarterly comparison is examined in isolation.

The slowdown becomes visible only when looking at annual totals. DGRO's total annual dividend per share for 2025 came in at approximately $1.45, compared to roughly $1.39 in 2024. That is an annual growth rate of 4.73%. The five-year dividend compound annual growth rate sits in a similar range. The stall is not about any single quarter being a disaster — it is about the compound growth rate at the annual level, which is the correct lens for income-focused investors.

Why the Morningstar Methodology Creates This Outcome

DGRO tracks the Morningstar US Dividend Growth Index. That index follows four core rules: companies must have at least five consecutive years of uninterrupted dividend growth; real estate investment trusts are excluded; the top ten percent highest-yielding stocks are screened out to filter dividend traps; and weighting is based on total dividend dollars paid rather than market capitalization.

The five-year consecutive growth requirement is where the structural issue begins. Five years is a permissive bar. A company that has raised its dividend every year but decelerated from 8% growth to 2% growth still qualifies. The index screens for continuation, not for growth rate acceleration. The result is a fund carrying a significant number of mature mega caps that technically clear the hurdle but contribute very little to distribution growth.

DGRO's top ten holdings — Exxon Mobil, Johnson and Johnson, JPMorgan Chase, Apple, AbbVie, Philip Morris, Procter and Gamble, Microsoft, Home Depot, and Merck — represent roughly 25% of the fund. Several pay dividends growing at 3% to 6% annually. Apple raises its dividend approximately 4% to 5% per year. Exxon, Johnson and Johnson, Merck, and Philip Morris have shown limited meaningful growth over extended periods. Because the index weights by total dividend dollars paid, these slower compounders receive heavier representation. The outcome — modest aggregate distribution growth — is a feature of the design, not a malfunction.

How SCHD's Quality Screens Produce Faster Income Compounding

SCHD screens for companies with at least ten consecutive years of dividend growth, along with filters for return on equity, free cash flow to debt ratio, and a quality composite score. It holds approximately 100 companies, compared to DGRO's roughly 400. That selectivity has produced a ten-year annual dividend compound annual growth rate of 10.99%.

SCHD's trailing twelve-month yield sits around 3.4%, versus DGRO's approximately 2.1% — a 60% income premium on the same dollar invested.

A $50,000 position in DGRO generates approximately $1,060 per year in dividend income. The same $50,000 in SCHD generates approximately $1,700 per year — a difference of roughly $640 annually. Applying SCHD's recent three-year dividend growth rate of 7.12%, a $50,000 SCHD position could produce roughly $2,400 per year in dividends within five years. The same DGRO position at 4.73% growth reaches approximately $1,330. The five-year cumulative income gap on a single $50,000 position exceeds $5,000.

For a broader look at how DGRO and SCHD work together within a structured dividend portfolio, see 4-ETF Dividend Ladder: How VIG, DGRO, SCHD & DIVO Pay $613/Month.

The Total Return Case for DGRO — and Why 2026 Is Different

Before treating this as a straightforward SCHD-wins conclusion, the ten-year total return data deserves attention. Over the past decade, DGRO delivered approximately 290% total return versus roughly 263% for SCHD. That gap is real and relevant for investors in accumulation mode.

DGRO's total return advantage has not come from its dividend growth engine — it has come from its growth-tilted holdings. The fund's inclusion of Apple and Microsoft, companies that qualify on dividend continuity while also compounding share prices at high rates, added meaningful price appreciation that pure income metrics miss. The lower yield on DGRO also results in fewer taxable distributions in non-retirement accounts, which supports net return over time.

The 2026 year-to-date picture tells a different story. SCHD is up approximately 12.79% while DGRO has gained roughly 1.57% — an 11 percentage point gap in just a few months. The market appears to be rotating toward the quality, income-oriented profile that SCHD's methodology emphasizes, and away from the growth-leaning mega caps that powered DGRO's past decade. The dividend growth stall and the price stall are two symptoms of the same underlying issue: DGRO's methodology is not adapting to the current cycle, while SCHD's is.

The March 2026 SCHD Reconstitution That Changed the Picture

SCHD's March 2026 annual reconstitution made significant changes to the fund's composition. Energy weighting dropped from roughly 20% to approximately 16.5%. Healthcare increased from around 16% to 18.5%. Consumer staples reclaimed the top sector position. UnitedHealth Group entered at the 4% individual stock cap. Qualcomm and Accenture gained additional weight.

The result is a fund profile that is more defensive and more tilted toward quality growth — a combination well-suited to 2026's flight-to-quality environment. DGRO's holdings did not go through a comparable refresh. Exxon, Johnson and Johnson, AbbVie, Merck, Philip Morris, and Procter and Gamble remain the primary drivers. SCHD's methodology structurally updates itself through annual reconstitution; DGRO's is not doing equivalent work in this cycle, and the year-to-date performance gap reflects that divergence.

Three Rotation Paths and the Tax Strategy Most Investors Skip

Investors holding DGRO in 2026 have three realistic options, each with different income and risk profiles.

Path 1 — Hold DGRO: At approximately $1,060 per year on a $50,000 position, applying the 4.73% recent growth rate produces roughly $1,330 per year within five years. Total return potential remains intact given DGRO's historical performance and 400-stock diversification.

Path 2 — Full rotation to SCHD: Immediate income rises to approximately $1,700 per year. At SCHD's recent three-year dividend growth rate of 7.12%, that position could reach $2,400 annually within five years. The trade-off is accepting SCHD's historically lower total return profile.

Path 3 — Split 50/50: A blended position produces roughly $1,380 in year-one income at an effective dividend growth rate near 6%. This path preserves DGRO's total return engine while adding SCHD's income acceleration, and avoids a binary call on which fund outperforms going forward. For most investors, the 50/50 split is the more practical answer.

Before executing any rotation in a taxable brokerage account, reviewing the tax lot structure is essential. Shares held longer than one year qualify for the lower long-term capital gains rate. Shares held less than one year are taxed at the ordinary income rate. Selling the oldest lots first and spreading the rotation across two calendar tax years are the two most effective ways to reduce the tax cost. Investors who prefer to avoid triggering any taxable event can stop new DGRO contributions and redirect all new cash into SCHD, allowing the allocation to shift naturally over time without a sale.

For investors within a decade of their target retirement date, The Dividend Bridge: Retire 10 Years Before Social Security covers additional frameworks for timing this kind of income transition.

Which Dividend ETF Belongs in Your Portfolio?

The decision framework for DGRO vs SCHD ultimately reduces to investment phase. For investors more than ten years from retirement who are focused on total return and wealth accumulation, DGRO remains defensible. Its 400-stock diversification reduces single-company risk. Its lower yield produces fewer taxable distributions in non-retirement accounts. And its total return track record is strong, even with dividend growth compressed.

For investors within ten years of retirement, or those shifting toward income distribution, the math increasingly favors SCHD. The 60% starting income premium compounds hard once distributions begin replacing earned income. A $200,000 position rotated from DGRO to SCHD at age 50 generates an estimated additional $2,500 per year in spendable income immediately — before dividend growth compounds that gap further over a 20-year retirement horizon.

DGRO is not a broken fund. It is a slow fund with declining dividend growth whose design served investors well during the 2010s. In the current cycle, the tighter, higher-quality, more concentrated profile of SCHD is outperforming. Whether that cycle continues is a data question, and the next two quarters of DGRO distributions — particularly Q2 2026, expected in June — will provide the next meaningful signal.

Watch the Full Breakdown on YouTube

For a complete visual walkthrough of the $50,000 rotation analysis, all three paths with five-year income projections, and the exact tax lot order for executing this strategy, watch the full video at the top of this page. The video includes the attribution breakdown showing how much of DGRO's historical return came from growth-tilted holdings versus its dividend engine — data that materially changes the rotation calculus depending on your investment phase.

This article is for educational purposes only and does not constitute financial advice. Always conduct your own research before making any investment decision.