- Key Takeaways

- How JEPQ Actually Generates Monthly Income

- Why JEPQ's Payout Has Risen Three Months Straight

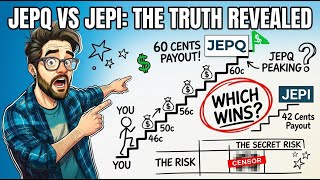

- JEPQ vs. JEPI: April 2026 Income Head-to-Head

- The Premium Pulse Rule: Three Signals Before Every Ex-Date

- Tax Drag: The After-Tax Reality of a 10.5% Yield

- The Bear Case: Concentration Risk and Total Return Reality

- Watch the Full Breakdown on YouTube

JEPQ, JPMorgan's Nasdaq-100-based covered call ETF, has just recorded its third consecutive monthly distribution increase. February delivered $0.4657 per share. March stepped up to $0.5090. April reached $0.5586. And the May ex-dividend date has already been declared at $0.60 flat — roughly a 30% increase in monthly income over just four months. The trailing twelve-month yield now stands at 10.51%, with an annual run rate exceeding $7.00 per share. A $100,000 position at the April ex-date generated approximately $1,006 in a single month. The critical question: is this momentum durable, or is a distribution compression coming?

Key Takeaways

- JEPQ's monthly distributions have climbed for three straight months: $0.4657 (Feb), $0.5090 (Mar), $0.5586 (Apr), with $0.60 declared for May 2026

- The 10.51% trailing yield is driven by option premium income via Equity Linked Notes, not traditional dividends

- A $100,000 JEPQ position paid approximately $1,006 in April 2026, compared to $737 for a comparable JEPI position

- Distributions rise when the VIX is elevated and compress when volatility calms — this is the core mechanism, not a flaw

- JEPQ distributions are taxed as ordinary income, reducing effective after-tax yield in high brackets to roughly 6.6%

- Six mega-cap tech names account for approximately 40% of JEPQ — it remains a Nasdaq-long position, not a bond substitute

How JEPQ Actually Generates Monthly Income

JEPQ launched in May 2022 under JPMorgan Asset Management with a 0.35% expense ratio — elevated versus passive index funds, but in line with actively managed products. As of early May 2026, the fund holds approximately $33.27 billion in assets under management.

The structure is what separates JEPQ from a standard ETF. Approximately 80–85% of the portfolio is held in direct Nasdaq-100 stocks. The remaining 15–20% is invested in Equity Linked Notes (ELNs) — structured products purchased from bank counterparties, including JPMorgan itself. Each ELN embeds a covered call written on the Nasdaq-100 index. When those calls expire, the premium collected flows to shareholders as the monthly distribution.

This means JEPQ distributions are not corporate dividends in the way SCHD or VIG payments are. They are option premium expressed as cash. Option premium responds to one variable above all others: implied volatility. High volatility means fatter premiums. Low volatility means thinner ones. Understanding this is the entire key to reading JEPQ's distribution history and anticipating its future payouts.

Why JEPQ's Payout Has Risen Three Months Straight

The VIX is the answer. During most of the second half of 2024, the CBOE Volatility Index sat in a calm 15–20 range. Then the macro picture shifted: a series of tariff-related announcements in late winter and early spring 2026 drove the VIX to spike repeatedly above 25. As of April 24, 2026, the front-month VIX future was trading near 20.80.

Three months of elevated volatility produced three months of rising ELN premiums, which produced three months of rising distributions. That is not a coincidence — it is the mechanism working exactly as designed.

The trailing twelve-month yield of 10.51% reflects the past twelve months. The 30-day SEC yield, which annualizes the most recent distribution against current NAV, is running closer to 12% based on the recent elevated payouts. Which measurement window you use determines the headline figure.

JEPQ's full performance record since inception illustrates the underlying pattern clearly:

- 2022 (May–Dec): JEPQ –12.89% vs. Nasdaq-100 –32.58% — the covered call structure cushioned the drawdown significantly

- 2023: JEPQ +36.28% vs. QQQ +54.86% — roughly 19 percentage points of upside surrendered

- 2024: JEPQ +24.89% vs. QQQ +25.58% — nearly identical

- 2025: JEPQ +15.19% vs. QQQ +20.77%

- 2026 YTD: JEPQ +4.25% vs. QQQ +8.21%

JEPQ outperforms in down markets, matches in neutral ones, and trails in strong rallies. The covered call caps upside participation — that is not a bug. It is the contract income investors are implicitly signing when they choose yield over capital appreciation.

JEPQ vs. JEPI: April 2026 Income Head-to-Head

Both JEPQ and JEPI are JPMorgan covered call ETFs using ELN structures, but they track different indexes — Nasdaq-100 and S&P 500, respectively. That distinction drives meaningfully different income levels depending on the volatility environment in tech versus broader large-cap equities.

In April 2026, JEPQ paid $0.5586 per share. At approximately $55.52 per share at the April ex-date, a $100,000 position is roughly 1,800 shares — generating approximately $1,005.50 in that single month. JEPI paid $0.4205 per share in April. At roughly $57.05 per share, a $100,000 JEPI position is approximately 1,753 shares, yielding about $737 for the same month.

JEPQ produced approximately $268 more per $100,000 invested in a single month. The premium reflects the higher implied volatility historically embedded in Nasdaq-100 options versus S&P 500 options. In a low-volatility environment where the S&P 500 holds steadier than the Nasdaq, that income gap could compress or reverse.

For investors building a structured income approach, pairing JEPQ with other income-oriented ETFs can create complementary cash flow streams. The 4-ETF dividend ladder using VIG, DGRO, SCHD, and DIVO offers a different volatility-income profile that pairs naturally alongside JEPQ's premium-driven distributions.

The Premium Pulse Rule: Three Signals Before Every Ex-Date

Rather than reacting to JEPQ's monthly payout after the fact, income investors can use three observable market signals to form a reasonable expectation before each ex-dividend date. Running these checks takes under five minutes and provides more actionable context than any single yield number.

Signal 1: 30-Day Average VIX

If the VIX has averaged above 20 over the trailing month, expect the next distribution near the high end of the recent range. If the trailing average drops below 17, expect a step down. Below 15 on a sustained basis, expect meaningful payout compression. A one-month VIX chart on any free financial site provides this data in seconds.

Signal 2: Nasdaq-100 Trend vs. 50-Day Moving Average

A whipsawing or range-bound Nasdaq-100 near its 50-day moving average expands implied volatility and inflates option premiums. A steady, low-drama uptrend compresses implied volatility and shrinks the premiums that flow to JEPQ shareholders. The index's price behavior is a direct leading indicator for the ELN income the fund will collect in the following month.

Signal 3: The Recent Payment Sequence

Look at the last six monthly distributions. A stair-stepping sequence — $0.4657, $0.5090, $0.5586, $0.60 — signals that volatility is consistently being priced into premiums and a momentum window is open. A zigzagging or declining sequence signals a regime unwind. The trend in the payment series itself carries predictive content about the next distribution.

Running all three signals in early May 2026: the VIX is near 20, the Nasdaq-100 is choppy and mixed, and the distribution series has climbed for four consecutive months. All three signals point toward a supportive premium environment for the May payment. Whether that momentum extends into June will depend on whether macroeconomic volatility persists or resolves through the summer.

Tax Drag: The After-Tax Reality of a 10.5% Yield

JEPQ's headline yield requires a tax adjustment before it can be meaningfully compared to qualified-dividend funds. Because most distributions derive from option premium income, the IRS classifies them as ordinary income — not qualified dividends. In a 37% federal bracket, investors keep approximately 63 cents per dollar received, reducing the effective after-tax yield to roughly 6.6%.

By comparison, SCHD's dividends generally qualify for the 15% preferential capital gains rate, netting about 85 cents per dollar. JEPQ still wins on absolute after-tax cash income at current yield levels, but the margin is narrower than the gross yield comparison implies.

Investors should also monitor JPMorgan's monthly 19a-1 notices, which estimate how much of each distribution is classified as ordinary income versus return of capital (ROC). ROC is not taxed in the year received — but it reduces cost basis, creating a larger capital gain at sale. Final income character is confirmed on the 1099-DIV the following February.

The optimal account type for JEPQ is a tax-advantaged structure. Inside a Roth IRA or 401(k), ordinary income treatment becomes irrelevant and distributions compound tax-free. For investors targeting income before traditional retirement age, JEPQ held inside a tax-sheltered account fits naturally into a dividend bridge strategy designed to fund living expenses before Social Security eligibility.

The Bear Case: Concentration Risk and Total Return Reality

JEPQ's income narrative does not change the underlying math on total wealth accumulation. The fund's top holdings mirror the Nasdaq-100's mega-cap concentration. As of early 2026: Nvidia at approximately 9.58% of the fund; Apple at 8.26%; Microsoft at 8.24%; Broadcom at 5.83%; Amazon at 5.06%; Tesla at 3.35%. Six names account for roughly 40% of the fund's total weight. A coordinated drawdown in those positions would drag JEPQ's net asset value regardless of ongoing option premium income flows.

On a total return basis, the comparison with QQQ is unflattering. Over the five-year period ending in late 2025, QQQ produced approximately a 106.68% total return. JEPQ produced roughly half that on a comparable window. Investors who deployed $100,000 into QQQ at JEPQ's May 2022 inception would have accumulated meaningfully more total wealth, even accounting for reinvested JEPQ distributions.

The income JEPQ generates is real and valuable — particularly for investors who need cash flow for living expenses or systematic reinvestment. But it is a cushion against drawdowns, not a hedge against them. JEPQ is a long-Nasdaq position with a covered call overlay that trades some upside for current income. Characterizing it as bond-like or low-risk misrepresents its fundamental structure and risk profile.

Watch the Full Breakdown on YouTube

For a complete visual walkthrough of JEPQ's distribution mechanics, an interactive JEPQ vs. JEPI income comparison, and a live application of the Premium Pulse Rule using current market data, watch the full analysis on the HF YouTube channel. The video covers the exact monthly payment timeline, four-year total return comparisons, VIX correlation data, and step-by-step signal interpretation — the fastest way to build a working mental model of how JEPQ behaves across different volatility regimes.

Disclaimer: This article is for informational and educational purposes only. Nothing here constitutes financial advice. Past distributions are not a guarantee of future payments. Always conduct your own research before making investment decisions.