- Key Takeaways

- The Three Rules Behind the 2026 Rebuild

- Foundation Layer: SCHD, DGRO, SCHG, and VTI

- Income Layers: Seven ETFs for Near-Term Cash Flow

- The Cost of Chasing Yield: A 35-Year Comparison

- Growth Layers: Six ETFs for Long-Horizon Investors

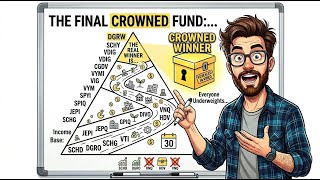

- The Crown Pick: Why DGRW Belongs at Every Age

- Watch the Full Visual Walkthrough

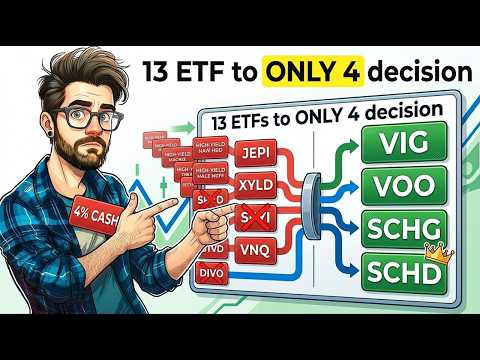

The dividend pyramid is one of the most practical frameworks in dividend investing, and the 2026 rebuild changes more than a third of its original selections. Six funds have been demoted, thirteen individual stocks have been replaced with ETF wrappers, and four brand-new funds — some launched after the original framework was first drawn — have earned permanent slots in the structure. The core principle remains unchanged: match every fund to its time horizon. The further from needing the money, the higher the position in the pyramid. The closer to spending it, the lower the layer.

Key Takeaways

- The 2026 pyramid replaces every individual stock with an ETF and ranks all 18 funds by time horizon, not yield size.

- JEPI's distributions fell more than 8% year over year; it now belongs only in a tax-sheltered account for near-retirees.

- Four new funds join the structure in 2026: SPYI, GPIQ, CGDV, and SCHY — with SPYI offering superior after-tax efficiency for taxable brokerage accounts.

- Chasing yield costs real money: $25,000 plus $500 per month compounded at 6% over 35 years reaches roughly $700,000 versus roughly $1.3 million at 8.5%.

- DGRW — yielding approximately 1.5% — is the single ETF every age underweights, with a historical annual total return near 14% over the past decade.

- Account placement is a first-order decision: ordinary income ETFs like JEPI belong in IRAs; SPYI's tax structure makes it more efficient in a taxable account.

The Three Rules Behind the 2026 Rebuild

Three rules govern every selection in the updated pyramid. First, every pick is now an exchange-traded fund rather than an individual stock — the original framework contained thirteen single-company positions, all replaced with ETF wrappers that provide access to the same underlying companies at lower concentration risk. Second, every layer has been stress-tested against the market crashes of 2020 and 2022 to reveal how each fund actually behaves when conditions deteriorate sharply. Third, every fund is ranked by a single variable: time horizon. The further from needing the money, the higher the position. The closer to retirement income, the lower the layer.

Foundation Layer: SCHD, DGRO, SCHG, and VTI

The foundation holds every portfolio at every age. For investors in their twenties and thirties, these four funds may constitute the entire portfolio for years. For investors at sixty, they remain the floor beneath all income-producing positions above them.

SCHD (Schwab US Dividend Equity, approximately $32.50 per share, 0.06% annual expense ratio) sits at the center of the foundation. It holds roughly 100 high-quality companies with consistent dividend payment histories. Its yield has compressed from nearly 4% to the low-3% range — somewhere around three and a half percent — as its price rose: more than $700 million flowed into SCHD in a single recent week. Its historically reinvested total return has ranged from approximately 9% to 13% annually depending on the measurement window, and it outperformed the broad market during the 2022 sell-off as capital rotated toward quality dividend payers.

DGRO (iShares Core Dividend Growth, 0.08% expense ratio) occupies the adjacent foundation slot. Unlike SCHD, whose yield compressed in 2026, DGRO's yield drifted upward from just above 2% toward the high-2% range, approaching 3%. It emphasizes companies accelerating their dividend growth rather than those already paying the highest yields, making it the natural growth-flavored complement to SCHD. For a detailed look at how these two funds compare, see DGRO vs SCHD: The Dividend Growth Stall Investors Need to See.

SCHG (Schwab US Large Cap Growth, 0.04% expense ratio) yields under 1%, which surprises many dividend investors. Its inclusion in a dividend foundation reflects a deliberate trade-off: for younger investors, capital growth is what funds future dividends. A 30-year-old who pours everything into high-yield funds today locks in income that cannot be spent for 35 years and surrenders the compounding that growth would have provided instead. In the 2022 crash, SCHG fell harder than any dividend fund in the pyramid because growth stocks take the deepest hit when interest rates spike — but it also recovered fastest, and its decade-long total return has meaningfully outpaced the income funds below it.

VTI (Vanguard Total Stock Market, 0.03% expense ratio) completes the foundation by covering the entire US market — more than 3,000 companies — in a single fund. It yields approximately 1.3%, so it is held not for current income but to ensure no single sector or position can sink the overall structure. VTI has tracked the long-term growth of the American economy for more than two decades and rebounded from every significant drawdown.

Income Layers: Seven ETFs for Near-Term Cash Flow

The income layers serve investors one to five years from converting a portfolio into a regular paycheck. These funds generate more income today; they also carry trade-offs the foundation does not. Account placement — taxable brokerage versus IRA or Roth — determines whether their distributions are tax-efficient or tax-expensive.

JEPI (JPMorgan Equity Premium Income) is the most demoted fund in the 2026 rebuild. When first included in the framework, it yielded above 8%. In the most recent year, its income fell by more than 8% year over year. The second problem is tax treatment: most of what JEPI distributes is classified as ordinary income, taxed at regular marginal rates rather than the lower qualified dividend rate. JEPI did cushion the 2022 crash better than pure equity funds — a real and meaningful advantage — but its appropriate role is now narrow and specific: near-retirement investors holding it inside a tax-sheltered account such as a traditional or Roth IRA, where ordinary income tax disappears.

JEPQ (JPMorgan Nasdaq Equity Premium Income) is the covered call fund that moved in the right direction in 2026. While JEPI's income contracted, JEPQ raised its payout by nearly 6% year over year and currently yields in the 10% range. Its technology-tilted underlying portfolio provides a different risk and income profile. The same tax caution applies — most of the payout is ordinary income — and the same account guidance holds: sheltered accounts only.

SPYI is one of four brand-new funds in the 2026 rebuild. It covers the 500 largest US companies with an options overlay and yields in the 11–12% range. What earns it a dedicated slot is tax structure: a large portion of its distributions receive significantly more favorable tax treatment than the ordinary income thrown off by JEPI and JEPQ. For an investor holding income ETFs in a taxable brokerage account, that difference can be worth several percentage points of real, after-tax yield every single year. Its expense ratio is approximately 0.68%, higher than the index funds in the foundation, but for the right investor in the right account it can be the most tax-efficient monthly income source on the entire list. SPYI is positioned as the income pick for the taxable account — the mirror image of JEPI as the pick for the sheltered one.

GPIQ (Goldman Sachs Income Builder), another new addition, has returned approximately 94% since launch compared to roughly 51% for a well-known older covered call fund over the same window — nearly double in the same period. Two important caveats apply: short-window performance figures can mislead when evaluating funds designed for multi-decade compounding, and GPIQ is young enough that it has not been tested through a sustained market downturn. Promising early performance is not proven durability.

DIVO (Amplify Enhanced Dividend Income) bridges income and growth by selling covered calls selectively against a focused set of high-quality dividend payers, rather than blanketing the full portfolio with options. It yields in the 6–7% range on a monthly basis, and its underlying dividend has historically grown at a healthy rate. For an investor approaching retirement who wants monthly income without the principal erosion associated with heavier covered call overlays, DIVO can balance current cash flow against continued appreciation. The 3-Bucket Dividend Strategy for Retirement shows a practical framework for how DIVO fits alongside growth-oriented positions in a near-retirement allocation.

VNQ (Vanguard Real Estate) adds an income stream that equities alone cannot replicate, historically yielding in the 3.5–4.5% range. Real estate fell harder than the broad market during the 2022 rate spike because rising rates directly compress property valuations. Most VNQ income is also taxed as ordinary income. It is best used as one diversifying slice within the income layer — an inflation-linked income source — rather than an anchor position.

HDV (iShares Core High Dividend, 0.08% expense ratio) closes the income layers as the defensive anchor. It holds a concentrated set of large, financially stable companies in energy, utilities, and consumer staples — businesses that continue paying dividends during economic contractions. It yields in the high-3% to 4% range, a level similar to where it sat when the original pyramid was drawn. Its concentration is both its strength and its risk: fewer holdings create more sector exposure, but also more defensive stability when markets deteriorate.

The Cost of Chasing Yield: A 35-Year Comparison

Before examining the growth layers, the failure mode math deserves direct attention because the numbers are striking. Consider two 30-year-old investors, each starting with $25,000 and contributing $500 per month for 35 years until retirement at age 65.

The high-yield investor, compounding at approximately 6% annually in covered call funds, could potentially accumulate around $700,000. The growth investor, compounding at approximately 8.5% annually in quality dividend growth funds, could potentially accumulate near $1.3 million — a gap of nearly $600,000 from identical contributions over the same period.

The high-yield investor also pays more tax along the way on ordinary income distributions, widening the real-world gap even further. This is the fundamental cost of parking in the income layers too early in a financial lifetime. Those layers exist for investors within five years of retirement — not for someone in their thirties with three decades of compounding still ahead.

Growth Layers: Six ETFs for Long-Horizon Investors

The growth layers reward patience over yield. A smaller payout that compounds fast outperforms a larger yield that stays flat over long time horizons, and every fund in these layers is built on that principle. Institutional money is already validating this shift: on a single recent Monday, more than $3 billion flowed out of pure growth and into quality dividend strategies — the same rotation this framework has mapped for years.

VIG (Vanguard Dividend Appreciation, 0.06% expense ratio) opens the growth layers. It yields approximately 1.75%, which causes income-focused investors to skip past it. That is a mistake: VIG's dividend has historically grown at roughly 9% annually, meaning the payout roughly doubles in under eight years without any additional capital. VIG also held up noticeably better than pure growth funds during the 2022 crash because dividend raisers tend to be mature, profitable businesses that attract capital during downturns.

VYM (Vanguard High Dividend Yield, 0.06% expense ratio) yields in the high-2% to low-3% range and is a legitimate fund — but it overlaps heavily with SCHD. Both target the same pool of large, high-yielding US dividend payers. Owning both does not add nearly as much diversification as two separate tickers might suggest. VYM functions best as a slightly broader alternative to SCHD rather than a true complement to it.

VYMI (Vanguard International High Dividend Yield, approximately 0.07% expense ratio) expands the income universe beyond American borders. International dividends often start at higher yields than US equivalents, and foreign markets can provide income when American companies are struggling. The trade-offs include less predictable dividend growth, extended periods of underperformance versus US markets, and more complex foreign withholding tax treatment — though much of that can be recovered as a foreign tax credit in a taxable account. VYMI addresses the home-country concentration risk that affects almost every US-based dividend investor.

CGDV (Capital Group Dividend Value) is the dark horse of the rebuild. Capital Group uses human judgment to select dividend payers rather than tracking an index mechanically, which can lower volatility and sharpen selection in the hands of a skilled team. On a single day in early May, the fund attracted approximately $463 million in fresh institutional money — inflows that signal serious professional interest. The honest caveat is that it is new, lacks a full market cycle of history, and requires trusting a management team rather than a rules-based methodology. It is the fund to monitor, not the one to anchor a structure around.

VDIG (Vanguard Dividend Growth) is Vanguard's direct response to SCHD, built to own quality companies with steady dividend growth records using Vanguard's low-cost index methodology. For the cost-conscious long-term investor, especially inside a tax-advantaged account, it is a legitimate complement or alternative to the foundation pick. As with VYM, checking the overlap with existing holdings before adding VDIG is essential — if it holds many of the same companies as SCHD, the diversification benefit is smaller than the separate ticker implies.

SCHY (Schwab International Dividend Equity, approximately 0.06–0.12% expense ratio) is the most underweighted pick among the runners-up for the crown. Almost every dividend investor carries heavy US concentration; SCHY adds international dividend exposure across both developed and emerging markets, reducing dependence on a single economy. There have been real multi-year periods when international stocks outperformed American stocks — a fact easy to forget after a long stretch of US dominance. Even a 10–15% allocation to SCHY meaningfully lowers that concentration risk. The trade-offs — slower historical dividend growth, more complex foreign tax treatment, and extended periods of underperformance versus US markets — are real, which is why it is the runner-up rather than the crown pick.

The Crown Pick: Why DGRW Belongs at Every Age

DGRW (WisdomTree US Quality Dividend Growth) earns the top position because it works across every layer of the pyramid simultaneously. It owns high-quality US companies screened for genuine profitability and consistent dividend growth, pays a monthly dividend yield of approximately 1.5%, and its distributions are qualified — taxed at the favorable dividend rate, not the ordinary income rate that reduces the real yield of JEPI and JEPQ. Its historical annual total return over the past decade has been in the neighborhood of 14%.

A hypothetical $100,000 investment compounding at roughly 14% annually for ten years could potentially grow to approximately $380,000. A comparable high-yield covered call fund compounding at 6% over the same decade might reach less than $200,000 — a gap of nearly $200,000 on a single position in just ten years. Stretched over a 35-year career, that gap does not grow linearly — it explodes.

What makes DGRW the universal pick rather than merely another growth fund is that it serves investors at every stage. It belongs in the foundation for a 25-year-old seeking decades of compounding. It works in the upper-middle layers for an investor in their forties or fifties balancing income against continued growth. It fits near the peak as patient capital with a long remaining horizon. No other fund on the list spans that range with the same combination of a growing, tax-friendly monthly dividend and strong long-term compounding speed. Covered call funds only fit the near-retiree. SCHG only fits the young. SCHY only corrects one specific blind spot. DGRW improves the speed of compounding paired with a gently taxed, growing monthly income stream for investors at every age simultaneously. That is the reason it stands alone at the summit of the 2026 rebuild.

Watch the Full Visual Walkthrough

The complete 2026 dividend pyramid — including crash-test results for all 18 funds, the live institutional money flows that mirror this exact structure, and the full visual layering comparison — is available in the video below. The layering logic, failure mode math, and fund-by-fund contrast are significantly clearer in visual format than in any written summary.

Watch: The Dividend Pyramid Rebuilt for 2026 (18 Picks for Every Age) on YouTube

Disclaimer: This article is for educational purposes only and does not constitute financial advice. All figures cited are historical returns or hypothetical illustrations. Always conduct your own research before making any investment decision.